Property management company vs self managing: compare costs, time, risk, tenant quality, and cashflow to choose the right rental strategy.

Continue readingProperty management company vs self managing: compare costs, time, risk, tenant quality, and cashflow to choose the right rental strategy.

Continue reading

What is property management services? Learn what managers handle, what owners gain, and when hiring support improves cashflow and reduces risk.

Continue reading

The Ontario Government has set the 2027 Rent Increase Guideline at 1.9%.

The rent increase guideline is not applicable to all rental units in Ontario. If you have questions about whether or not the guideline applies to you, please don’t hesitate to reach out to us for clarification.

As a reminder about Rent Increases:

You can learn more about the guideline and associated rules and regulations here: 2027 Rent Increase Guideline

No matter how hard you work to be a great Landlord or choose a great Tenant, things don’t always go as planned.

The Landlord and Tenant relationship can be complex, with competing priorities sometimes leading to conflict and disputes. Add to that the fact that Life happens…people lose jobs, people get divorced, repairs get overlooked, damage gets done. The job of being a Landlord can be perilous and you can easily find yourself a difficult situation with your Tenant. That comes with the territory.

When things do go wrong, the most important priority is to take correct action immediately. That’s half the battle. The thing is, it’s not always easy to know what the correct action is. In fact, it can be downright overwhelming and stressful.

In our experience, the worst thing that you can do in any situation is to guess at the correct course of action. Guessing means that you’re not making an informed decision based on experience. Guessing means that you’re at a higher risk of making the wrong decision, which could (and usually does) worsen the situation.

The same goes for us at East Vista. We have an experienced Paralegal firm on retainer, to advise us when we’re unsure or in doubt. Even though we have years of experience, we still encounter situations that we’ve never dealt with before. That’s just part of the business. In cases like these, it’s critical that we are sure of the correct course of action. A consultation with our Paralegal is a critical component of making the right decision and getting the best outcome.

We always recommend that a Landlord get help if or when they are in doubt about what to do in a given situation. As Property Managers, we can help with most situations, but often what the Landlord really needs is proper legal advice and/or legal action. Yes, there is a cost to going the legal route, but the benefits far outweigh the costs.

We believe that success as a Landlord depends on having a strong support network, which should include an experienced Paralegal. Getting expert advice and guidance will help you to avoid the guesswork and take swift, correct action in any situation.

East Vista Property Management offers Paralegal services for any situation. You can also learn more or find a Paralegal through the Law Society of Ontario here.

Non-payment of rent is likely the single biggest fear of every Landlord. With no rent coming in, Landlords quickly feel the financial strain of carrying the costs of the property on their own.

As if the financial strain isn’t enough, Landlords must also contend with significant delays in the legal process to resolve the non-payment issue. Since the onset of the pandemic, the backlog of cases at the Landlord and Tenant Board has ballooned to 53,000 cases, according to a March, 2024 report. Non-payment of rent issues are now taking upwards of 8-12 months to resolve.

It seems like a dire situation, but that doesn’t mean that you are powerless. Resolving a non-payment of rent issue is all about being proactive and taking action quickly when a problem arises.

In our experience, rent payment issues generally fit within five levels of severity. Each level has an appropriate course of action:

The Tenant proactively contacts you to say that their rent will be late and gives you a definite date on which it will be paid. They then pay on or before that date as promised.

Usually nothing to worry about, but might indicate that their finances are fragile and are living paycheque to paycheque. Best to cut them some slack if they’ve been a good Tenant, which can help to build goodwill. However, if it starts to happen more often, you’ll need to take a stricter approach to the keeping them on the payment schedule.

What to do:

Communicate with the Tenant and let them know that you can give them some extra time this month, but going forward they need to be on-time, as per their lease agreement. Send a friendly payment reminder a couple of days before their next rent payment is due.

The Tenant’s payment behaviour starts to become erratic or unpredictable. They start to develop a habit of paying late.

At first, this will seem like a minor issue. You trust the Tenant and know that they have good intentions and will pay as soon as they’re able. Eventually though, this will become the norm and you’ll start to feel that the Tenant is taking advantage of your goodwill. This payment pattern can easily slip into a more serious issue.

What to do:

Maintain an open line of communication with the Tenant and follow up on payment frequently. Silence on your part is worse thing that you can do, as it takes the pressure off the Tenant. If they don’t hear from you, they’ll assume that you’re ok with the situation. If the behaviour persists, start the RTA process outlined below, by serving the Form N4. That might be enough to let them know you’re serious and they’ll get their payments back on schedule.

The Tenant starts paying in instalments randomly throughout the month without your consent.

This is a more serious issue that warrants a more aggressive response.

What to do:

Start the RTA process outlined below as soon as their full rent payment is not received. In many cases, the N4 will be voided by the end of the month assuming they pay in full. That’s ok. Start the process again if their rent is late the following month. Yes, it’s a lot of paperwork and can seem like the Tenant is gaming the system, but your effort will pay off. If the payment behaviour persists and you have the history of N4s, you can seek eviction for constant late payment of rent. That route is not always successful, but will likely help to get the Tenant back on their payment schedule.

The Tenant starts to accumulate arrears.

This is where the slope becomes slippery. Arrears can accumulate quickly (especially with today’s high rental rates!), to the point where the Tenant is not able to catch up. It’s important that you take action as soon as any arrears are carried over to the next month.

What to do:

Start and follow the RTA process outlined below immediately. No matter what the Tenant’s story is, or how good your relationship has been, start the process without hesitation. If the Tenant pays the arrears and voids the N4, great! But if things start to spiral downwards, you’ll be in a great position to get the legal process going with the L1 Application before the arrears accumulate too much.

The Tenant stops paying rent and becomes difficult to get in touch with.

In our experience, this usually does not happen out of the blue, as there are usually indicators as described in points 1 to 4 above. The Tenant may be upset about some other issue (eg. unresolved maintenance issues) or may have experienced a traumatic even (eg. a job loss). In most cases, there is a change in behaviour leading up to this scenario that the Landlord should have been aware of. The non-payment of rent is basically the bottom of a downward spiral that has been happening for some time.

What to do:

Hopefully, you’ve already started the process by serving the N4. If not, don’t wait and hope that the situation improves. It likely won’t. If the Tenant is not communicating, then submit the L1 Application to start the legal process.

The biggest mistake we see Landlords make is letting the unacceptable payment behaviour continue too long before taking action. This might be because they have a good relationship with the Tenant and want to help them out, or they just procrastinate because they don’t know how to handle the issue correctly, or they falsely believe that the situation will improve.

The problem is: with today’s high rental rates, the arrears accumulate so quickly. Realistically, if a Tenant hits 2 month’s of arrears it’s highly unlikely that they’ll be able to catch up.

If you haven’t started the legal process by that point, then you’re heading for a world of hurt, as it could take 4-6 months to just get a hearing with the LTB, then another 2-3 months until the actual eviction date. That could potentially mean almost a year without rent. It happens just that easily.

The best course of action is to start the legal process immediately by following the RTA process outlined below. Even if the Tenant does pay their rent in full and restarts the process, at least you’ve demonstrated that you are serious and will take action.

There are specific steps you should follow, as outlined by the Ontario Residential Tenancies Act (RTA). Apart from the backlog at the LTB, the system does work if everything is done correctly.

1. Serve a Notice of Non-Payment of Rent

– Form N4 (click here to access the N4 and Instructions published by Tribunals Ontario)

– This form can be served to the Tenant the day after rent is due.

– It provides the Tenant with 14 days to either pay the overdue rent or move out (19 days if sending the notice by mail).

– Clearly and correctly state the amount of rent owed and the period it covers. The amount owed must be rent only, not other arrears, such as Utilities.

– Send the notice by an allowable means of delivery. Email delivery is permitted only if the Tenant has consented in writing, which should be specified in the Ontario Standard Lease Agreement. You can read our overview and learn the most important clauses of the Lease Agreement Here.

2. Wait for the Notice Period to Expire

– If the Tenant pays the rent within the notice period, the notice becomes void.

– If the Tenant does not pay the rent or move out within the notice period, the Landlord can proceed to the next step.

3. File an Application to Evict a Tenant for Non-payment of Rent and to Collect Rent the Tenant Owes

– Form L1 (click here to access the L1 and Instructions published by Tribunals Ontario)

– This form is used to request a hearing with the LTB to seek an eviction order and to collect the rent owed.

– The application can be submitted online or in person, and there is a fee associated with filing ($186.00 at the time of writing).

4. Attend the LTB Hearing

– Both the Landlord and tenant will be notified of the hearing date.

– The Landlord must present evidence of the unpaid rent and any communications with the tenant.

– The Tenant is given the opportunity to explain their situation.

– The Landlord and Tenant may negotiate a repayment plan, which can be a win-win. The Landlord is able to collect the arrears owing and the Tenant avoids eviction. One condition of the agreement is that the Tenant is automatically evicted if they are late with a payment.

5. Receive the Decision

– If the LTB rules in favor of the Landlord, an eviction order will be issued (if a repayment agreement was not feasible).

– The Tenant will have an opportunity to pay the rent owed and void the eviction order, usually within 11 days (referred to as the “standard 11-day void period”).

– If the Tenant does not pay within this period, the eviction order becomes enforceable.

6. Enforce the Eviction Order

– If the Tenant still does not pay the rent owed after the LTB decision, the Landlord can request the Sheriff to enforce the eviction order.

– Only the Sheriff can legally remove the Tenant from the rental unit.

7. Collecting Unpaid Rent

– If the Tenant owes rent even after vacating the property, the Landlord can take further steps to collect the debt, such as hiring a collection agency or seeking garnishment of wages.

– In our experience, this can be very challenging. For one thing, if the Tenant had the money, they likely would have paid their rent to avoid eviction, so collecting it afterwards will be difficult. Secondly, it can be difficult to track them down once they’ve moved out. Thirdly, they can claim bankruptcy to avoid repayment altogether.

We always recommend that a Landlord should hire a reputable Paralegal to represent them throughout this process. Yes, there is a cost to legal representation, but the benefits far outweigh the costs:

Having a Tenant not pay their rent can be a stressful situation, but that doesn’t mean that you are powerless. In any scenario, you need to take quick and correct action to minimize your risk and losses.

By following the process outlined above, you’ll be able to resolve many issues yourself. You’ll also be in a position to swiftly take legal action if the problem persists or worsens.

Like anything, it’s impossible to control the behaviour and actions of others, but by preparing yourself for action, you protect yourself against negative outcomes.

Finding a high-quality Tenant begins with effective marketing of your rental listing.

What do we mean by effective marketing?

It’s the process of attracting your ideal Tenant. Anyone can post a Listing on Facebook and Kijiji, but there’s a process involved in creating a high-quality Listing that will attract the right Tenant, not just any Tenant.

You want your rental unit to be appealing to potential Tenants and stand out from other rental listings on the market. Always remember that the quality of the property determines the quality of the Tenant.

In the interior, ensure the property is thoroughly cleaned and any necessary maintenance or repairs are completed. On the exterior, cut the grass and remove any unnecessary clutter (e.g. recycle or garbage bins). Strive to improve the curb appeal, to make a good first impression in your photos and during Showings.

If you have an existing Tenant living in the property, there is only so much that you can do. If they have given proper notice to vacate, they are obligated to cooperate with the listing/showing process. However, that doesn’t mean that they will necessarily keep the rental unit in the condition that you expect for Showings, nor are they obligated to (they have a right to quiet enjoyment).

The best course of action with existing Tenants would be to ask them politely to help you out, by keeping their unit clean and decluttered. During showings, inform the candidate that the unit will professionally cleaned and list the repairs and upgrades that will be completed before they move in. The rental unit may not show well with a Tenant living there, but potential applicants may look past that if they know that it will be in good condition when they take possession.

Hire a professional photographer to take high-quality photos. Good lighting and angles can make a significant difference in how attractive the property appears in listings.

Professional photos will help you to stand out in the crowd compared to competing rental listings in the area. A good set of professional photos will cost approximately $150.00, but you’ll have them on hand for future listings.

Research similar properties in the area to understand the going rental rates. Online platforms like Facebook Marketplace, Realtor.ca and Kijiji.ca can provide insights into local market conditions.

Be realistic in your expectations. Rental rates are market-driven, not cost-driven. This means that rental rates are determined by the characteristics of the local market, not your monthly carrying cost of the property.

At a basic level, the rental rate must be comparable to similar units available for rent in your market.

You must also consider affordability. What can Tenants realistically afford to pay for rent in your area? Consider their lifestyle and other expenses they are juggling, such as: Utilities, fuel, groceries, car payments, etc?

Determining a correct rental rate is not an exact science. It’s more like an educated guess. The key is to be aware of the feedback you’re receiving and adjust accordingly. For example, if the rental rate is too high, there will be very little interest in the property. You should try reducing the price to stimulate traffic on your listing.

Write a detailed description highlighting the property’s features, amenities, and any unique aspects. Include information on nearby schools, public transport, shopping centers, and other local amenities.

Also include details about what information the candidate needs to provide as part of the application process. For example, we require ‘recent proof of income, a recent Credit Report and Photo ID’.

Avoid application requirements that are unreasonable or could be seen as discriminatory or illegal. Do some research ahead of time, to ensure that you comply with Ontario Laws.

Once you’ve created a compelling listing and obtained a great set of photos, it’s time to put it all together and create your rental Ads.

Today, it’s easier than ever to reach your ideal Tenant candidates. Most of the advertising options are free of charge and reach a large audience depending on where you’re located. There are also a couple of paid-advertising options, that can achieve a larger targeted reach.

What are some of the best advertising platforms?

There are also a few platforms that provide a wider reach, but come with a cost:

Inform friends, family, and colleagues that you have a rental property available. Personal referrals can be very effective. You likely know someone that knows someone that’s looking for a place.

If the property is located on a high-traffic street, then a high-quality sign is a great way to raise awareness about your listing. Reach out to a local sign shop to have a simple yet professional sign made for you. The cost is minimal and will look much more professional that a hand-written one.

Once your Ads are posted, you should start to receive enquiries immediately. The amount of traffic that you receive is a good indicator of how well you are positioned in the market. If you only receive a trickle of interest, then your rental rate might be a little high or you might need to expand your reach with paid advertising. Monitor the traffic for one to two weeks, then adjust accordingly.

Finding a great Tenant is a competitive game. Every other Landlord wants them, so you need to move fast to get them before they do.

Your response should be polite and professional, more like business communication as opposed to chatting with a friend. In the early stages, avoid phone calls and stick with written communication with the candidate, at least until you meet them for a Showing.

One important note: You must avoid getting sucked into the drama in someone’s life. You’ll have people send you long explanations about their situation, which can be a red flag. Some of their stories can be heartbreaking and you will naturally want to help. But you must remember that the drama is usually a pattern in that person’s life and will eventually affect you and your rental business. Best course of action is to not respond and move on.

The moment that you connect with a potential candidate is the moment that your Tenant Screening process starts.

You can learn more about our process for effectively screening and selecting a potential Tenant HERE.

Attracting the right Tenant for your property begins with creating a high-quality Listing that will set you apart from the competition. It does take extra effort and some expense, but the quality of your Listing will have a direct impact on the quality of your applicants.

As every Landlord knows, being a Housing Provider is both rewarding and challenging. At times, it can feel like a rollercoaster of emotion, as things can go from calm to crisis at any moment. It can be difficult to manage the fluctuating demands of the property, especially with all the other demands in your life.

On a daily basis, we see Landlords that are overwhelmed, discouraged, frustrated and tired. This state of mind can create a downward spiral of procrastination, indecision and indifference, which can damage their relationship with their Tenant and negatively impact the financial performance of the property.

It doesn’t have to be this way!

The most successful Landlords realize that they can’t do it all themselves. They get help with the most critical elements of the rental business by building a team of experienced professionals that can handle any challenge.

Finding a good Tenant is your highest priority as a Housing Provider, but most Landlords don’t have the time, patience or tools necessary to do it properly. This can lead to short-cuts and bad decisions when it comes to choosing a Tenant.

Getting help with finding a Tenant will pay off in many ways. For example, a Property Manager will do the legwork of vetting candidates and present you with the best potential Tenant. This will save you time, effort and the stress associated with finding the right fit for you and your property. A good Property Manager will also stand behind their Tenant selection by offering a guarantee to reduce your risk.

Learn more about our Tenant Screening process HERE.

Being a Housing Provider means that you’re on-call 24/7 for your Tenants.

As a Landlord, it’s important that you be responsive and proactive when it comes to maintenance and repairs. This can be a challenge for some Landlords, as they might not have the experience or expertise to know what to do, or they may not live anywhere near the property.

Ideally, you should have a network of contractors and trades at your disposal, including:

Of course, you can’t predict every issue, but having these contractors at your fingertips will cover 95% of the issues that arise. Another option is to hire a Property Manager, as they already have a network of contractors in place and can respond quickly when the need arises.

What do I mean by ‘correctly’?

Owning a rental property and being a Landlord is a business. You’re offering a product to the market (your rental unit), to solve a need (Housing) in exchange for money (Rent) to a Customer (Tenant). Like any business, there are certain rules, protocols and standards, either real or implied, that must be done correctly for a business to be successful.

This is even more critical in the rental business, as Housing plays such an important role in your Tenant’s life (and all of Humanity for that matter). I would go as far as to say that Housing forms the foundation of our Society.

In our interactions with Tenants:

Operationally:

Sometimes things just don’t go right. That’s the reality and risk of being a Housing Provider.

When things do go wrong, it’s important that you take swift and correct action, so that the problem doesn’t escalate. For example, if a Tenant stops paying their rent, or has damaged their unit, or has a dispute with a neighbouring Tenant, swift action is needed to correct the problem and hopefully get things back on track.

Depending on the situation, it can be difficult to know what the correct action is. Most Landlords end up guessing and blundering their way through it, which often makes things worse.

The correct course of action in any situation is to not guess, but to get help or advice from someone with experience. A Property Manager can help, but a good Paralegal is also an essential part of your team. Yes, hiring a Paralegal does come at a cost, but it will save you loads of time, money and stress. An experienced Paralegal is invaluable, as they know how to navigate the legal system, to get issues resolved quickly and efficiently.

One other thing to consider: If the issue does go to a hearing at the Landlord and Tenant Board, the Tenant will be provided Duty-Council free of charge. That means that you’ll be pleading your case against an experienced Paralegal. This can put you at a disadvantage as they know the laws and how to navigate the system for the benefit of the Tenant.

Getting help with key elements of the rental business is critical for success as a Landlord. Trying to do everything yourself might save you money in the short-term, but can end up costing you lost time and money and increased stress. Get professional help and keep your rental business on the right track!

The simple answer is Yes!

Many Landlords are indecisive when it comes to giving their Tenant an annual rent increase.

On one hand, their costs are going up every year, but on the other hand, they don’t want to rock the boat and risk losing a good Tenant.

I’ve been there. We were in the same situation with the Tenants at our first rental property. They were a fantastic young couple and took good care of the property. They paid their rent on time and were a pleasure to deal with, so we didn’t increase the rent for many years.

The problem is, eventually the rental rate is way behind the market rate. In our case, we were $500/month behind. Money’s not everything, but eventually you start looking at what you’re getting vs. what you could be getting. When it gets to that point, you kinda start wanting the Tenant to leave, even though they’re a great Tenant.

The Tenants finally gave notice to vacate after about 7 years of renting from us. I feel a little guilty in saying it, but we were glad that they were moving on, as we’d be able to get the property back up to market rent. They were fantastic Tenants, but it definitely would have been a better experience for us if we had increased the rent throughout the tenancy.

The lesson for me was: It’s important that a Landlord consider the needs of the Tenant and foster a positive Landlord-Tenant relationship (which we got right), but the Landlord also needs to balance that with protecting their own best interest, so that the relationship is mutually beneficial.

Many Landlords are happy with their nice, stable Tenants, so are hesitant to increase the rent because they don’t want to “rock the boat”. They fear losing the Tenant and the associated costs of finding a new Tenant, plus the risk of a vacancy or getting a bad Tenant next time.

Landlords will also rationalize that the amount of the allowable rent increase (for most units in Ontario the maximum is 2.5% in 2024). However, you need to consider the long-term.

A great position to be in for sure, but still, the property is an asset and should be performing at peak capacity. The Landlord should consider Return on Capital and what it looks like if they ever decided to sell the property. A low rental rate could have a negative impact on the selling price.

As the property owner, your costs will go up every year, guaranteed. Your Property Taxes, Insurance, Maintenance costs, and maybe even your borrowing costs will go up. That means that you’re essentially making less money as time goes by.

Market rental rates generally trend upwards, so you can soon find that your rental rate is hundreds of dollars behind the market rate. Your Tenants will also see this and will be less likely to move out because their costs will be higher for the next rental unit. They know they have a good deal and will sit tight.

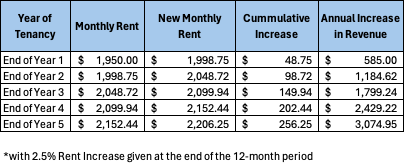

As you can see in the table below, even small rent increases compound over time. This can have a significant impact on the financial performance of the property over the years. The allowable rent increase may not keep pace with the market, but at least you won’t be too far behind.

In general, most Tenant expect that the rent will go up each year and accept it. If the Landlord and Tenant are on good terms, then the likelihood of a rent increase causing a Tenant to leave is highly unlikely.

As I mentioned in my own story, the Landlord-Tenant relationship must be mutually beneficial. Fostering a great relationship with your Tenant by not increasing the rent is an admirable quality, but you might eventually resent the Tenant because their rental rate is so low and they have no plans on leaving any time soon. You’ll start feeling like you’re being taken advantage of, even though it was your choice not to increase the rent over the years.

The risk of losing a Tenant is low, as they will likely not be able to find anything cheaper. Tenant’s keep a close eye on the market and know if they’re at, above or below the market rental rate.

If they’re generally happy with their rental unit and have good relationship with their Landlord, they are unlikely to look elsewhere. Finding and moving to a new place is costly and time-consuming for the Tenant (plus the risk of getting a bad Landlord). As long as the rent increase is reasonable, it makes more sense for them to stay where they are.

No, it doesn’t.

In Ontario, a minimum of 12 months must pass between each rent increase and Tenants must be given 90-days notice using the N1 Form. But that doesn’t mean that you must give a rent increase every 12 months. You can give an increase every 15 or 18 months, if that makes more sense for you.

This is where it can get tricky.

In Ontario, most rental units that were built after November, 2018 are not subject to Rent Control. That means that a Landlord is free to increase the rent as much as they want.

In this scenario, we always suggest that the Landlord keep the increase to a reasonable amount, say 5%. This amount seems reasonable to the Tenant, yet still gives a significant bump in revenue to the Landlord.

The challenge we’re seeing today is that because the property owner paid such a high price for the property in recent years, most find it difficult to maintain a positive cashflow. So when the time comes for the annual rent increase, many will base the increase on the carrying costs of the property. We’ve seen rent increases in the range of $300 – $500 per month. Not because the Landlord is spiteful, but because their costs are so high and the property is a financial drain on their personal finances. Unfortunately, for the Tenant the Tenant doesn’t have much choice in this scenario, except to find a cheaper place to live.

Yes, there are circumstances where it makes more sense to forego the rent increase:

Real Estate works in cycles, so there may be times when supply of rental housing in the area exceeds demand. This can drive rental rates down, which means that Tenants have more options and might even be able to save a few dollars by moving to a less expensive rental unit.

If your current rental rate is at or near the market rate, then you might want to reconsider giving a rent increase. As your rate starts to creep above the market rate, Tenants will naturally start looking for something less expensive.

Events like the recent pandemic or the closing of a local Employer can have a significant effect on the rental market.

In these situations, you should shift your focus to Tenant Retention, as turning a Tenant during these periods would be costly and you’re less likely to obtain a higher rental rate.

In general, we strongly encourage our Clients to increase the rent within the allowable limits annually. The risk of losing a good Tenant is low and Landlords need to do all they can to ensure that they’re not falling behind every year. It’s just good business and beneficial to both the Landlord and the Tenant in the long run.

In todays rental environment, Tenants have higher expectations of their Landlord than they did in the past. I don’t mean that they are more demanding, but they do have higher expectations in terms of living standards, fairness and most importantly: Responsiveness.

The rental business has changed and Housing Providers must recognize that there is now a Customer Service element to the rental business. The Tenants of today are paying significantly higher rents, have higher living standards, have more selection of rental units available and are a more educated group of consumers than ever before. The Tenant should now be viewed as a Customer, with the Product being the rental unit and the ‘after-sales service’ that’s provided by the Landlord. Responsiveness is a fundamental element of good Customer Service and Landlords need to embrace this.

Our culture has also changed. All of us expect things to happen instantly. Whether it’s texting a friend or ordering food delivery, we expect quick response and swift action. We pretty much have zero tolerance for waiting for anything and Tenant expectations are no different.

But being responsive goes beyond good Customer Service or keeping the Tenant happy; it’s a fundamental aspect of property management that also impacts property maintenance, legal compliance, and the financial performance of the rental unit.

Responsiveness contributes significantly to Tenant satisfaction. When Landlords promptly address concerns, Tenants feel valued and respected, leading to a more positive rental experience. Satisfied Tenants are more likely to stay in place, reducing turnover costs and stabilizing income for the Landlord.

Quick responses to maintenance requests prevent minor issues from escalating into major problems. Timely repairs help maintain the property’s condition and value, reducing the risk of costly repairs down the line.

Landlords have legal obligations to maintain safe and habitable living conditions for their Tenants. Prompt responses to issues related to health, safety, conflict and maintenance help Landlords fulfill these obligations and avoid legal liabilities.

Responsive landlords tend to have higher Tenant retention rates. Tenants are more likely to continue with their Lease if they feel their concerns are addressed promptly and their living environment is well-maintained. Less Tenant turnover reduces costs and stabilizes the revenue of the rental unit.

Word-of-mouth can significantly impact a Landlord’s reputation, especially with the advent of Landlord-Tenant Forums on Social Media. An upset or dissatisfied Tenant can make can cause quite a stir online, which can impact a Landlord’s ability to find good-quality Tenants in the future.

Delayed responses to maintenance issues or tenant complaints can result in financial losses. For example, prolonged vacancies due to Tenant dissatisfaction or property damage from neglected maintenance can affect rental income and property value.

Respond to tenant inquiries, requests, and concerns in a timely manner. Whether it’s via phone, email, or an online Property Management software platform, being accessible and responsive shows that you prioritize Tenant satisfaction.

Quickly address maintenance issues and repair requests. Establish a system for Tenants to report problems and ensure that these issues are resolved promptly to maintain the habitability and safety of the rental property.

Make yourself or your property management team accessible to Tenants when needed. Provide clear contact information and establish communication channels for Tenants to reach out with questions or emergencies.

Anticipate potential issues and take proactive steps to address them before they become major problems. Conduct regular inspections of the property to identify maintenance needs and address any issues promptly.

After addressing tenant concerns or completing repairs, follow up with Tenants to ensure that the issue has been resolved satisfactorily. This demonstrates your commitment to tenant satisfaction and reinforces trust and goodwill.

Establish clear policies and procedures for Tenants to follow when reporting maintenance issues or seeking assistance. Ensure that Tenants understand how to contact you or your property management team and what to expect in terms of response times.

Show empathy and understanding towards Tenants’ concerns and situations. Building positive relationships with Tenants fosters a sense of trust and encourages open communication.

Overall, being a responsive Landlord involves being proactive and attentive to the needs of your Tenants. Do that and you’re well on your way to fostering a positive rental experience and a well-functioning, financially stable rental property.

Lack of proper communication with Tenants can lead to a range of negative outcomes for Housing Providers, ranging from Tenant dissatisfaction and increased Tenant turnover to legal issues and financial loss.

So many issues and conflicts are caused by the intent and tone of a message being misconstrued by the Receiver. Short, abrupt Text Messages, poor grammar and language barriers can often cloud the true intent of the message.

As a best practice, the Sender should reread the message and consider it from the viewpoint of the Receiver, then edit the message to ensure that it makes sense and has the right tone.

Selecting the correct communication channel is also critical, not only for effective interactions with your Tenant, but also because the Residential Tenancies Act may specify that certain actions are communicated in a certain way.

Text Messaging can be a quick and convenient way to communicate with a Tenant but tends to be less professional. In some cases, an email message or hard-copy letter by mail is more appropriate and might even be required by law (eg. serving Notices)

There is no hard and fast rule, but prompt response to a message is just good business and shows respect and empathy towards the Sender.

Clear and effective communication helps in maintaining a positive landlord-tenant relationship. When tenants feel heard and understood, they are more likely to be satisfied with their living situation, leading to longer lease durations and lower turnover rates.

Good communication allows landlords to address any concerns or issues raised by tenants promptly. This can prevent minor problems from escalating into major disputes and helps in maintaining the property in good condition.

Landlords have legal responsibilities towards their tenants, as outlined in the Residential Tenancies Act, in terms of behaviour, responsiveness and how to serve Notices. Proper communication ensures that landlords fulfill these obligations in a timely manner, reducing the risk of legal disputes. Learn about the most relevant clauses within the Act here.

Clear communication about rent payment expectations, due dates, and accepted payment methods can help ensure consistent and timely rent collection. It also facilitates transparency, reducing misunderstandings and disputes related to rent payments.

Regular communication with tenants allows landlords to stay informed about any maintenance issues that need attention. Timely maintenance not only preserves the value of the property but also enhances tenant satisfaction and retention.

In case of emergencies such as fire, flood, or other disasters, effective communication protocols enable landlords to quickly communicate important information to tenants and coordinate necessary actions for their safety and well-being.

Open communication channels encourage tenants to provide feedback on their living experience, which can help landlords identify areas for improvement and make necessary adjustments to enhance the property and overall tenant satisfaction.

Landlords can improve communication with tenants in several ways:

Provide tenants with multiple communication channels such as email, phone, text messaging, and a designated online portal for reporting issues or asking questions.

Respond promptly to tenant inquiries, requests, and concerns. Acknowledge receipt of messages even if a resolution will take time, to reassure tenants that their communication is valued.

Keep tenants informed about relevant information such as upcoming maintenance schedules, property improvements, or changes in policies. Regular newsletters or email updates can be effective for this purpose.

Utilize property management software or apps that allow for easy communication, maintenance requests, and rent payments. These platforms streamline communication processes and provide a centralized hub for tenant interactions.

When communicating important information or decisions, provide written documentation such as notices, letters, or emails to ensure clarity and avoid misunderstandings.

Foster transparency by openly sharing information about rent increases, status of repairs, property inspections, and any other relevant matters that may affect tenants.

Encourage tenants to provide feedback on their living experience and actively listen to their suggestions, concerns, and complaints. Address any issues raised and take appropriate action to improve tenant satisfaction.

Maintain a professional demeanor in all communications with tenants, even in difficult situations. Respect their privacy, confidentiality, and rights as renters.

After resolving an issue or addressing a concern, follow up with the tenant to ensure that they are satisfied with the outcome and to reinforce the importance of open communication.

By implementing these strategies, landlords can establish effective communication practices that enhance tenant satisfaction, promote a positive landlord-tenant relationship, and contribute to the overall performance of the rental property investment.

In this series of 8 articles, we explore the 8 biggest mistakes that we see Landlords make and how to avoid them. Click on the links below to read the previous articles:

Landlord Mistake #1 – Selecting the Wrong Tenant

Landlord Mistake #2 – Not Running the Numbers